Size of the Universe

As at July 2019, African eurodollar and local currency sovereign bonds, bills and notes had a total value of around USD 0.5 trillion1.

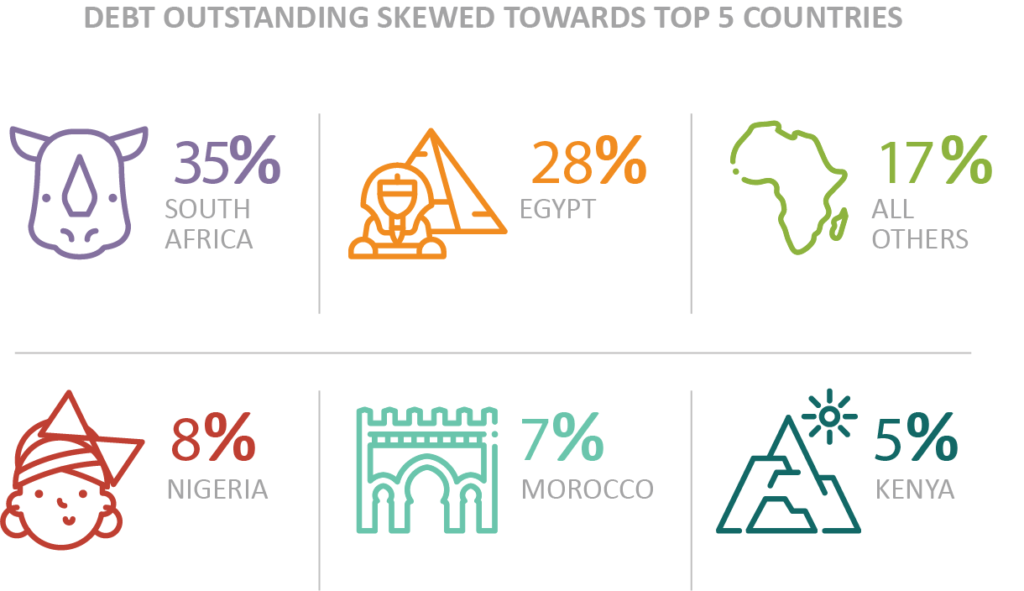

South Africa and Egypt make up the most substantial portion of bonds outstanding at, 35% and 28%, respectively.

Source: Bloomberg, RisCura analysis

Only three countries on the continent have an investment-grade credit rating (South Africa, Botswana and Mauritius).

South Africa and Egypt have the third and second lowest value of bonds outstanding, respectively. Only Mexico is lower.

Bonds outstanding to GDP is below 60% for all the African countries. The higher the debt to GDP, the more a country is exposed to credit risk. Although there is no optimal debt-to-GDP ratio, the IMF highlights that high debt to GDP ratios can cause the debt to become unsustainable.

Egypt has the highest bonds to GDP percentage at around 60%. In Egypt, the local currency bonds as a percentage of GDP is sitting at approximately 49% with foreign currency bonds at the remaining 11%. When looking at South Africa, the total bonds to GDP is sitting at around 51% with local currency debt and foreign currency bonds making up 47% and 5% as a percentage of GDP, respectively.

Despite having one of the biggest bond markets across frontier markets, Nigeria has a low bond debt to GDP ratio at 11%.

Africa has a larger number of frontier markets compared to emerging markets. Frontier markets in the continent are analysed together and compared to Bangladesh, Jordan, Serbia and Croatia. Croatia has the biggest bond market followed close by Nigeria and Morocco at USD 42.6bn, USD 41.9bn and USD 40.4bn, respectively. Botswana and Guinea Bissau have the smallest bond markets across the frontier markets, both sitting at USD 1 billion. Despite having one of the biggest bond markets across frontier markets, Nigeria has a low bond debt to GDP ratio at 11%. Morocco has a slightly higher bond debt to GDP at 34%, but lower than that of Mauritius and Croatia at 46% and 70%, respectively.

1Note: Data could not be reliably gathered for the following African countries: Algeria, Cape Verde, Central African Republic, Comoros, Democratic Republic of Congo, Djibouti, Eritrea, Ethiopia, Guinea,Liberia,Libya, Mauritania, Niger, Republic of Congo, Sao Tome and Principe, South Sudan and Sudan.