Energy

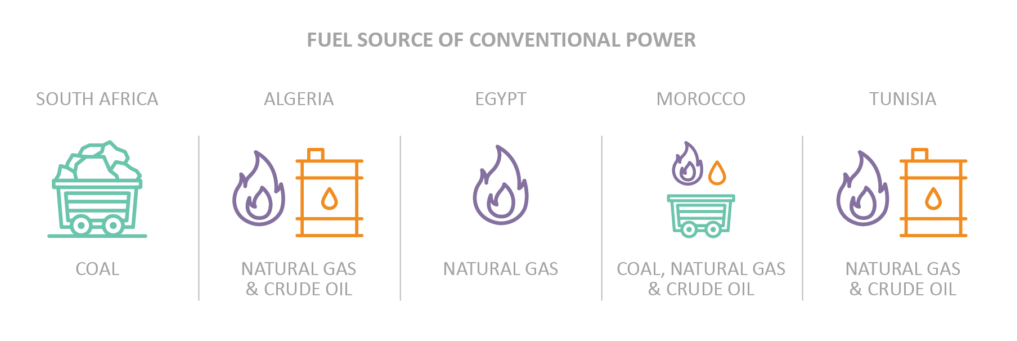

The more advanced, industrial economies of South Africa and North Africa have the largest installed capacity on the continent. Although conventional thermal power makes up the bulk of capacity in these markets, the primary fuel source differs by market.

Source: TradeMap, RisCura analysis

* Capacity factor= Production (KWH) / Capacity (MW) x 1000 x 365 x 24

[Note: Capacity factor not available for Francophone West Africa due to incomplete data.]

Even though Egypt’s power production capacity is higher than South Africa’s, they produce about 15% less energy than South Africa. This is because they have a lower capacity factor, meaning that they convert a lower percentage of their potential power resource into usable energy. Different types of electricity generating technologies have different capacity factors. For example, solar and wind plants have a generation capacity of around 20%, due to the sun not shining 24 hours a day and the wind not constantly blowing. In comparison, nuclear and fossil fuel-driven thermal technologies have much higher averages of around 75% and 45% worldwide (Source: U.S. Energy Information Administration).

However, considering the power capacity mix of Egypt compared to South Africa and the Maghreb, their capacity factors should all be close to 45%, with the high exposure to conventional thermal power. Similarly, Nigeria’s energy production is operating below its potential, with only a 30% capacity factor. Reasons for a lower capacity factor could be constrained resource availability to run the plant, age of infrastructure and downtime caused by maintenance, or lower efficiency of technology, among others. The lower capacity factor in these markets means a relatively smaller investment is needed to upgrade existing capacity to achieve significant increases in production, compared to other markets that would need to invest in brand new capacity.

There is good potential for growth in the use of renewable energy on the continent.

According to the U.S. Energy Information Administration, less than one million people are without access to electricity in North Africa. However, in sub-Saharan Africa (excl. SA), the picture is very different.

An alternative option which has gained traction over the past few years is small-scale solar installations that are financed by private companies and paid off as the infrastructure is used.

The question of demand for additional energy per capita is an interesting one. We don’t believe that investment in energy capacity is expected to substantially increase the amount of electricity that the general population uses in a short space of time, particularly in rural areas. The cost and time to build distribution networks in these areas are not always viable. An alternative option which has gained traction over the past few years is small-scale solar installations that are financed by private companies and paid off as the infrastructure is used.This removes the need for transmission and distribution networks covering thousands of kilometres into rural Africa.

Approximately 70% of planned and ongoing infrastructure projects are publicly funded, with about 25% set up as public-private partnerships, and the remaining 5% operating privately.

Additionally, the lack of reliable power on the continent acts as an inhibitor to certain energy intensive industries. Local companies are unable to compete with imports due to the high cost of running a factory on generators. A reliable power source would enable new, value-additive industries to develop on the continent. Importantly, this energy does not necessarily have to come from a national grid and utility company. In countries where energy generation is open to private parties, captive power plants can offer a cheaper and more reliable alternative with private partners, who develop their plants and distribution lines within a localised area.

Approximately 70% of planned and ongoing infrastructure projects are publicly funded, with about 25% set up as public-private partnerships, and the remaining 5% operating privately.